Bahrain’s real estate sector continues to grow despite lower YoY activity

- In 2023, the value of real estate trading decreased by 1.2% YoY to reach BHD 1.1Bn, while the volume of transactions grew by 24.1% YoY.

- While the residential sector declined slightly, the retail, industrial, and office sectors remained stable, with minor rental drops in the office sector.

- Bahrain recorded a GDP growth of 2.4% in 2023, a decline compared to 4.9% in 2022. However, a projected annual real GDP growth of 3% in 2024 is expected, driven by the non-oil sector, and aiding the real estate sector.

The latest Bahrain real estate report by Savills shows that Q1 of 2024 saw 6,124 sales transactions, marking a 3% drop compared to the same period the previous year.

In 2023, the value of real estate trading slightly decreased by 1.2% to BHD 1.1Bn versus 2022. However, the volume of real estate transactions jumped 24.1% in the same period.

Bahrain recorded a slight decline in GDP growth in 2023 compared to 2022, however, the Ministry of Finance and National Economy projects an annual real GDP growth of 3% in 2024, driven primarily by the non-oil sector, alongside other main contributors such as Financial Corporations, and the Manufacturing sector.

Despite these challenges, the real estate sector continues to grow, driven by government support, rising investor confidence, and an increasing demand for real estate in the region, according to Hashim Kadhem, Head of Professional Services.

Residential Sales & Rental Market

Home buyers are becoming more strategic in the market, primarily focusing on mid-range properties, and the availability of more affordable housing options with improved amenities has shifted the market dynamics in favour of tenants, the report says.

“Bahrain’s coastal location and flourishing high-end tourism industry continued to drive demand for luxury waterfront properties, which appeal to buyers seeking exclusivity and comfort,” Kadhem said.

A stream of projects is expected to be handed over in 2024, which could further widen the gap between demand and supply and potentially affect capital values in the short term. In Q1, the capital values of apartments grew slightly by 0.3% QoQ, primarily due to the growth in high-end apartment units, averaging 832 BHD/sqm. Factors such as tighter liquidity conditions, lower loan-to-value ratios, and higher lending rates have affected the demand for premium developments, particularly villas. High-end villas saw a year-on-year dip of 4.5% in capital values, averaging at 583 BHD/sqm.

Some of the most significant completions in the first quarter of the year included Onyx Residences by Kooheji Development, Al Nasseem Phase 2 Villas by Diyar Al Muharraq, and Wadi Al Riffa by Bareeq Al Retaj, among others.

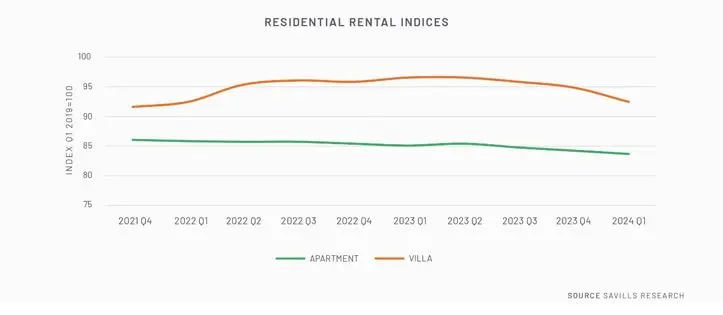

Overall rental values in the residential sector recorded marginal dips compared to Q4 2022, with rents across apartments declining by 1.3% and villas by 1% YoY. Low-end property rents dropped by 5.6% YoY and are now estimated at BHD 425/month, mid-end properties slipped by 3.5% YoY to BHD 493/month, and high-end properties saw a marginal annual increase to BHD 649/month.

Office Sales & Rental Market

The office sector experienced a quiet period during Q1 2024, with businesses renewing leases in high-quality Grade A properties. Rental rates for high-end offices now average at BHD 6.4, slightly higher than mid-end at BHD 6.3, and low-end offices at BHD 4.1 per/sqm/month. This has led to a 1.8% YoY rental contraction. Capital values for Grade A properties remain stable due to an increase in supply, with completions like Sayacorp, Future Generation Reserve Tower, and Seef Boulevard expected in the near term. Low-end properties in the Capital Governorate experienced a 6% drop in capital values QoQ. Financial services and government entities were key space takers, with an increase in demand for LEED-certified office spaces. Co-working spaces are also in high demand, particularly from startup companies and businesses looking to downsize.

Retail Rental Market

For the fourth quarter in a row, retail rental rates have maintained stability due to the festive seasons, a surge in mall footfalls, the government’s efforts to draw tourists, and significant infrastructure investments. The mall and mixed-use development rentals remained stable and are at BHD 12.3 and BHD 7.9/sqm/month, respectively. Strip retail rentals, however, have dropped by 1% YoY.

Industrial Rental Market

The manufacturing sector is the primary driver of demand in the industrial market, with an average space occupancy ranging from 1,500 to 3,000 sqm. In Q1 2024, despite an increase of 1.2% YoY in rentals, average rental rates for large and medium-sized warehouses have remained steady.

About Savills Middle East:

Savills plc is a global real estate services provider listed on the London Stock Exchange. With a presence in the Middle East for over 40 years, Savills offers an extensive range of specialist advisory, management and transactional services across the United Arab Emirates, Oman, Bahrain, Egypt, and Saudi Arabia. Expertise includes property management, residential and commercial agency services, property and business assets valuation, and investment and development advisory. Originally founded in the UK in 1855, Savills has an international network of over 700 offices and associates employing over 40,000 people across the Americas, UK, Europe, Asia Pacific, Africa, and the Middle East.

For further information, please contact:

Savills press office:

+971 50 316 5605 amjad.mkayed@savills.me

+971 50 331 5460 siddhi.sainani@savills.me

+971 (0)4 365 7700 www.savills.me

Email: info@cyber-gear.com

Email: info@cyber-gear.com